Looking Out for Fraud: What Attorneys Need to Know

Occupational fraud continues to wreak havoc on businesses, with annual business losses reported to exceed $4.7 trillion worldwide. Fraud experts have long suggested that the presence of three conditions, known as the “fraud triangle,” greatly increases the likelihood that an organization will be defrauded.

The classic fraud triangle, as conceived by criminologist Donald Cressey, consists of Pressure, Rationalization, and Opportunity.

The Fraud Triangle, Cressey

The Fraud Triangle, Cressey

Pressure

A perpetrator experiences some type of pressure that motivates fraud. Pressure can come from within the organization – for example, pressure to meet aggressive earnings or revenue growth targets. Alternatively, the pressure could be personal, such as the need to maintain a high standard of living, pay off debt, medical bills, or gambling.

Rationalization

Perpetrators often mentally justify their fraudulent conduct. They might tell themselves that they’ll pay back the money before anyone misses it, or reason that:

- They’re underpaid and deserve the stolen funds,

- Their employers can afford the financial loss,

- They’ll lose everything (or someone) if they don’t commit fraud,

- “Everybody” does it, or

- No other solution or help is available for their problems.

Most employees who commit fraud are first-time offenders who don’t view themselves as criminals, but as honest people caught up by circumstances beyond their control. By rationalizing, perpetrators overcome ethical barriers that generally guide their conduct.

Opportunity

Without opportunity, even motivated and rationalized perpetrators can’t commit fraud. Occupational thieves exploit perceived opportunities that they believe will allow them to go undetected. Weak internal controls, oversight, and auditing create opportunities for fraud. Addressing these issues is the best way to prevent fraud since it’s within the organization’s control.

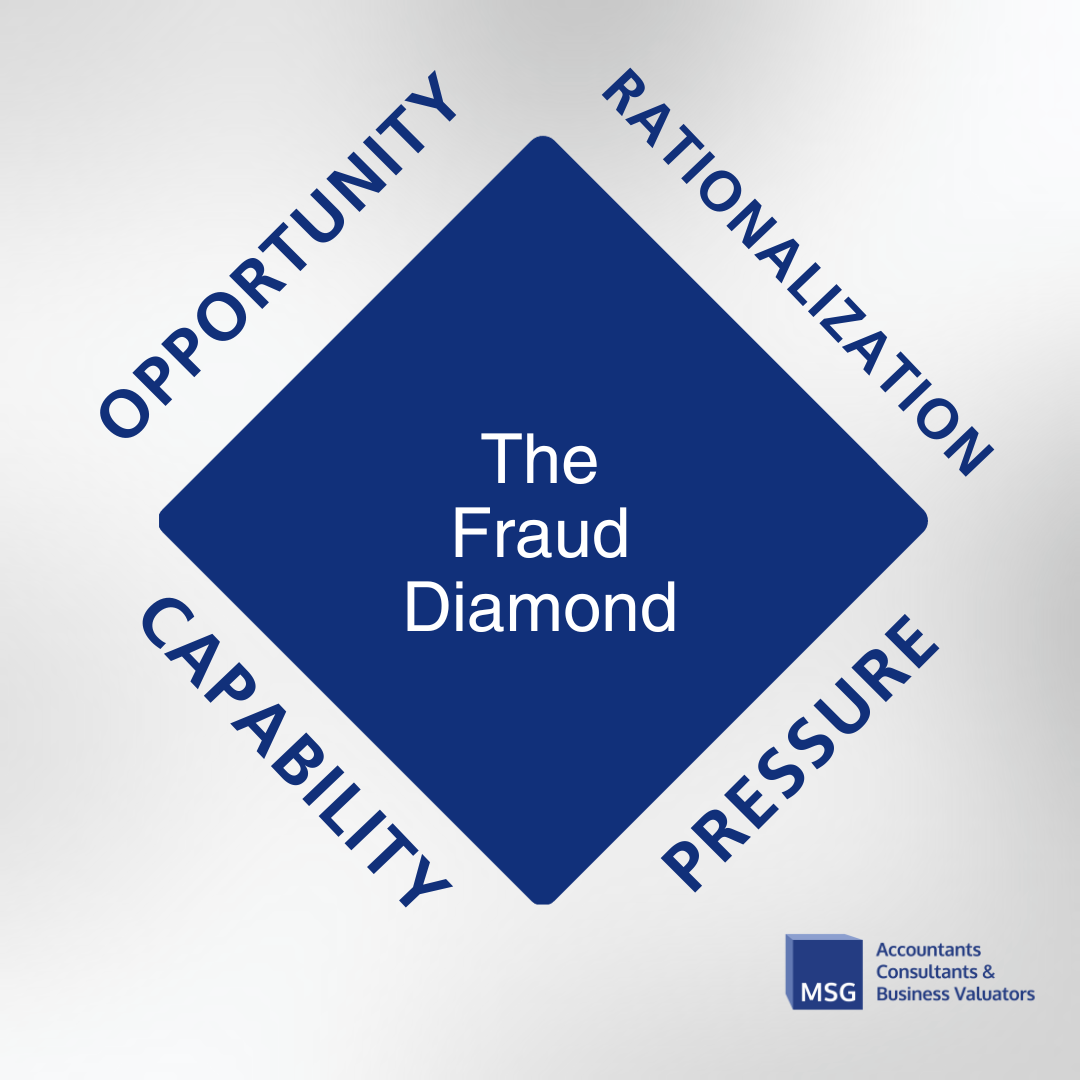

Other Fraud Models

The Fraud Diamond, Wolfe et al.

Since Cressey’s original fraud configuration, other experts have proposed expanding the conceptual framework to account for societal influences, integrity, arrogance, competence, personal greed, and employee disenfranchisement. While one or more of these conditions may be present, the most widely supported addition is what’s being called capability. So, the three-angled triangle may be replaced with a fourth item to create a “fraud diamond.”

Not every employee with motivation, rationalization, and opportunity commits fraud. Some people are more capable of unethical actions without guilt or stress. Capability involves many factors, including position, intelligence, confidence, resilience, and persuasion skills.

The MICE (Money, Ideology, Coercion, and Ego) model shares similar considerations with the fraud diamond. MICE retains the original three sides of the fraud triangle but shares the opportunity leg with a second triangle with sides for criminal mindset and arrogance.

Fraud perpetrators with characteristics matching the original motivation, rationalization, and opportunity triangle are categorized as “accidental fraudsters” – those who wouldn’t commit fraud without motivation. Those on the side of the criminal mindset, arrogance, and opportunity triangle are deemed predators or pathological fraud perpetrators. These individuals require only opportunity.

Red Flags

It’s important to remember that the conditions discussed above don’t constitute proof that fraud has been committed – or that an individual will commit fraud. Instead, the fraud triangle and its variants are designed to help organizations identify risk and understand the importance of eliminating the perceived opportunity to commit fraud.

Our firm frequently gets involved in fraud examinations when specific triggers are identified. These “triggers” may include:

- Unusual Cash Balances: This could be a notably low cash balance in an account that has historically been sufficient for the organization’s needs.

- Missing Assets: Instances where valuable assets have mysteriously disappeared or can’t be accounted for.

- Drastic Revenue Declines: A sudden and significant drop in revenue that defies typical patterns.

- Material Expense Category Changes: Any substantial alterations in one or more expense categories can be an early sign of financial irregularities.

If you suspect your client’s business is being defrauded, schedule a 15-minute case discovery call with Mark S. Gottlieb, CPA/ABV/CFF, ASA, CVA, CBA, MST.