When valuing a closely held, private company, it is important to recognize that the process may be more complex than valuing a publicly traded one. While valuation experts apply discounts at both the entity and shareholder levels, this blog will focus on exploring the various types of shareholder-level discounts and their impact on the valuation of closely held companies. Shareholder-level discounts are applied specifically to the value of an individual shareholder’s interest, accounting for the unique risks and limitations associated with owning a specific ownership interest. These discounts are used in the valuation process to arrive at a more accurate representation of the fair market value of a shareholder’s interest. Discount for Lack of Marketability (DLOM) Selling shares and liquidating funds is not as simple for a private company as for a publicly traded company. In a public company, shareholders can typically sell their shares on a stock exchange and receive the proceeds within a few days. However, this is not the case for closely held companies, where selling shares can be lengthy and complex due to the lack of a readily available market. The discount for lack of marketability is one of the most frequently applied discounts in valuing closely held companies. This discount reflects the difficulty of selling or liquidating ownership interests in a private company compared to a publicly traded one. The DLOM is used to account for the limited liquidity of closely held company shares and the potential difficulty in finding a buyer. Additionally, legal and […]

Blog

Category: Business Valuation

We have distilled decades of experience at the intersection of law, business and finance into a suite of articles to help our clients make sense of business valuation, forensic accounting, and litigation support. Please visit our site regularly for our latest content.

Shareholder-Level Discounts in Valuing Closely Held Companies

Posted in Business Valuation, on Apr 2024, By: Mark S. Gottlieb

Share

How the Market Impacts Closely-Held Business Valuations

Posted in Business Valuation, on Mar 2024, By: Mark S. Gottlieb

Share

When valuing any business, one of the most important factors to consider is the overall market environment. After all, market conditions have an enormous influence on a company’s performance and what buyers are willing to pay. Privately owned businesses have more protection from immediate market fluctuations than publicly traded companies. But over the longer term, market forces always make their way into financial statements and operational health. In a strong, growing economy, valuations tend to be more generous when demand is high and access to capital is easy. Buyers have more confidence that a target business will continue thriving, allowing them to forecast future solid cash flows. This leads them to place higher multiples on a company’s earnings. Of course, the reverse is true in weaker, uncertain economies as well – buyers become more conservative in their projections, and valuations reflect that uncertainty. Market swings can impact industries and niches very differently, too. For example, a recession may completely deflate valuations of discretionary consumer businesses like gift shops when households pull back spending. As we saw during the result of the pandemic, demand for discount retailers and certain services may remain stable or even grow during downturns. Evaluating the market’s impact requires a nuanced, segment-by-segment analysis in addition to big-picture economic factors. An accurate business valuation must determine how the current market will likely affect future operations. As experts, we analyze historical performance, competitive forces, supplier costs, commodity prices, consumer demand, access to labor, and other external variables that impact […]

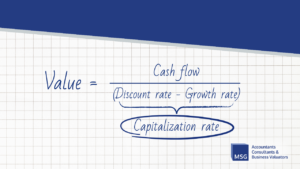

Scrutinizing The Capitalization Rate Within A Business Valuation Report

Posted in Business Valuation, on Feb 2024, By: Mark S. Gottlieb

Share

When representing a client with a business valuation report in hand, attorneys must look beyond the numbers at face value. Though you often leave the financial modeling and technical details to the valuation experts, a keen understanding of valuation inputs remains imperative for attorneys on either side of a transaction or dispute. The capitalization rate (a.k.a. the “cap rate”) is among the most impactful business valuation inputs. This factor warrants particular scrutiny, as variations of even 0.5 percent can alter the valuations significantly. Properly vetting this input is essential to achieve an accurate valuation that stands up to legal scrutiny. To add another instrument to your toolbelt, we will provide a quick primer on the cap rate and its components. What is the Capitalization Rate? The capitalization rate is the rate of return used to convert a business’s annual earnings or cash flows into an initial company value, accounting for risk and growth prospects. Computed as the difference between the discount and growth rates, the cap rate involves a nuanced evaluation of multiple factors. Attorneys should be familiar with these items to interpret their credibility quickly. Discount Rate The discount rate is the annual rate used to convert projected future cash flows into present value, reflecting the riskiness, time value of money, and required rate of return an investor would expect on the investment. The most common components used when computing the discount rate are: Risk-free rate of return Equity risk premium Size Premium, and Company-specific risk premium Generally, empirical […]

Detecting ‘Window Dressing’ Tactics in M&A Valuations

Posted in Business Valuation, on Jan 2024, By: Mark S. Gottlieb

Share

As a business valuation expert, I am often called in to assess the true value of a business that is the target of an acquisition. In many such deals, there’s an intricate dance between financial reality and manipulated appearances, which may present a glossier, more appealing image of a company’s financial health than what reality might reveal. In a recently reported case between two private equity firms, the acquirer alleged the seller employed multiple accounting gimmicks to inflate the earnings of a software company, Mobileum, prior to its $915 million sale. By prematurely booking revenues and masking expenses, they claim the target’s profits were artificially inflated by over $250 million. While the allegations remain in dispute, they underscore risks I regularly highlight to clients. As we evaluate the financials of an M&A target, here are some manipulative techniques that our team looks for. Premature Revenue Recognition Illegal yet common, this ploy involves recording future anticipated revenue as current-period income, inflating top-line figures before a sale. Sellers may book forward years of subscription revenue, excessive sales to partners, or less commonly, fictitious sales from shell companies to portray accelerated growth. Capitalizing Expenses This tactic converts regular operating expenses into long-term capital expenditures, enabling costs to be depreciated over years instead of impacting the income statement immediately. By reclassifying expenses as assets without proper documentation, companies reduce reported expenses, inflate reported assets, and subsequently increase profits and net worth. Channel Stuffing A risky tactic, channel stuffing involves shipping surplus products to distributors […]

How Lower Valuations Can Sweeten the Deal for Employees

Posted in Business Valuation, on Oct 2023, By: Mark S. Gottlieb

Share

Twitter, or “X”, taken private after Elon Musk’s $44 billion acquisition just over a year ago, is now valued at only $19 billion. A new internal memo is cited offering employees restricted stock units (RSUs) at a share price of $45. When private companies offer stock-like compensation options, the IRS advises them to use a 409A valuation – an independent assessment of how much a company is worth. These appraisals tend to be more conservative than valuations based on recent funding rounds or offers from potential acquirers, for example. X itself is “still negative cash flow,” Musk shared in July, citing a “50% drop in advertising revenue plus heavy debt load”. So, it’s not unsurprising that X’s 409A valuation came in lower than the $54.20 per share that Musk paid to take the company private. Because of this conservative approach, it’s common for companies’ 409A valuations to come in lower than their previous private market valuations. Last year, Stripe and Instacart saw their valuations slashed by 28% and 38%, respectively after new 409A appraisals. There are a few reasons why private companies incentivized by employee stock compensation may actually prefer to have lower 409A valuations: Lower strike prices on stock options give employees more potential upside and incentive to join and stay. With a lower valuation, the same number of shares granted or optioned to employees represents less dilution percentage-wise for existing shareholders. Companies can reduce stock-based compensation expenses with a lower 409A valuation. Employees only pay taxes when they […]

Plotting Your Client’s Financial Finish Line: Exits for Entrepreneurial Retirees

Posted in Business Valuation, on Oct 2023, By: Mark S. Gottlieb

Share

As the baby boomer generation continues to reach retirement age, with 10,000 individuals turning 65 every day, the United States is facing a “silver tsunami” of business owners looking to exit their companies. This mass exodus of entrepreneurial talent has made exit planning for retirees an increasingly pressing issue, especially for closely-held businesses. When advising clients on retirement and ownership transition, forensic accountants and business valuators provide invaluable expertise by highlighting crucial financial considerations that can profoundly impact the success of the process. In this blog post, we will explore five key points that business owners should keep top of mind when starting their exit plans. From stock options and business valuations to tax implications and ESOPs, our goal is to provide attorneys and their clients with the financial clarity needed to help navigate the choppy waters of retirement and ownership transition. Stock Options: Stock options are a cornerstone of exit planning. Clients must grasp the significance of these financial instruments, and this is where the expertise of forensic accountants and business valuators becomes crucial. These professionals can elucidate the nuances of restricted stock, stock appreciation rights, and employee stock ownership plans (ESOPs), shedding light on the potential advantages and disadvantages of each option, including intricate details such as control retention and tax implications. Business Valuation: The accuracy of business valuation is paramount in exit planning. Forensic accountants and business valuators possess the specialized skills required to determine the true value of a business. Their expertise in employing diverse […]

Legal Consequences of Inflated Valuations: Trump Case and Beyond

Posted in Business Valuation, on Sep 2023, By: Mark S. Gottlieb

Share

Yesterday, New York Supreme Court judge Arthur Engoron ruled in the ongoing lawsuit alleging former President Donald Trump and his businesses provided false financial statements to obtain loans and other benefits. This case piqued my interest as a credentialed business valuation expert, forensic accountant, and expert witness. Yesterday’s decision was over thirty pages long, and I wanted to break down the extent of the document for those following these ongoing legal battles. The New York Attorney General’s office had brought claims against President Trump, his family members, and corporate entities under a statute prohibiting persistent fraudulent conduct in business. The AG submitted evidence that President Trump inflated the valuations of his assets on financial statements from 2011 to 2021. For instance, President Trump claimed his apartment in Trump Tower was 30,000 square feet, later learned to be about three times its actual size. This overstatement led to an overvaluation of over $100 million! The Court also found evidence that other Trump assets, such as branding premiums, shared the same misstatement. President Trump’s legal team asked the Court to dismiss the entire case, arguing the financial statements contained disclaimers and that determining value is subjective. Those requests were later denied. The Court ruled yesterday that the Attorney General provided sufficient evidence that President Trump knowingly submitted false financial statements over multiple years. The judge ordered the dissolution of several corporate entities owned by the Trumps and the appointment of an independent monitor for the Trump Organization. While further potential penalties […]

Five Key Considerations When Valuing a Business in a Shareholder Dissolution Case

Posted in Business Valuation, on Aug 2023, By: Mark S. Gottlieb

Share

For the better of the past two years, we have been working on a shareholder buyout dispute centered on the value of a fifty percent interest in a business and its ability to support the buyout provisions. The shareholder’s agreement outlined the valuation standard and the terms of its payment. Despite this direction, each party’s valuation proposed at arbitration was millions of dollars apart. I will save the particulars of this case for another time but share with you that the value opined in our report was accepted in the arbitrator’s binding decision. One of the reasons for this favorable business divorce case outcome was that our client’s attorney respected our focus on essential valuation fundamentals. In return, his direct case and cross-examination led to a well-versed presentation of the issues at bar. Attorneys tend to many issues in a shareholder dissolution case; having a command of opposing valuation reports is just one. Here are five key considerations attorneys should consider when reviewing their experts’ reports and those of the opposing side. 1. Standard of Value The choice of a standard of value is fundamental to the valuation process. Two common standards often considered are fair market value and fair value. Fair market value is defined in Revenue Ruling 59-60 of the Internal Revenue Code: The amount at which the property would change hands between a willing buyer and willing seller, when the former is not under any compulsion to buy, and the latter is not under any compulsion to […]

Treasury Yields Are Increasing: How Does This Impact The Valuation of Closely Held Businesses?

Posted in Business Valuation, on Aug 2023, By: Mark S. Gottlieb

Share

Have you seen the bank advertisements looking to lure account holders to open short-term CDs at 4.5% or 4.9%? You may have read this article in the Wall Street Journal tracking the increasing treasury bill rates over the past few months. Where is this coming from, and how will this recent increase in Treasury Yield rates impact the valuations of closely held businesses? Figure 1. Adapted from Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis. FRED | St. Louis Fed. The short answer to this question: It may profoundly impact various aspects of the economy – including the valuations of closely held businesses. The complex relationship between financial variables can reverberate across different sectors. We will delve into the mechanisms behind some of these interactions and explore how rising treasury yields can influence the valuation landscape of closely held businesses. Treasury Yields 101 First, it’s essential to understand what treasury yields are and how they function. Treasury yields represent the expected return from investing in government bonds. This return is often called a “risk-free rate” since the government guarantees it. When yields rise, it generally indicates that the market demands higher compensation for lending money to the government due to factors like inflation and changes in monetary policy. Discount Rate And Present Value An increase in treasury yields directly affects the computation of the discount rate and, in turn, affects the valuation of closely held businesses. In business valuation, the discount rate is […]

What To Consider In Determining Owner’s Compensation

Posted in Business Valuation, on Jan 2021, By: Mark S. Gottlieb

ShareWhether a company is being valued for a shareholder or an equitable distribution dispute, one of the most common normalization adjustments to a subject company’s income stream is owner compensation. Both the Court and the IRS tend to closely scrutinize this issue, with the IRS in frequent disagreement as to the reasonableness of shareholder-employee compensation. For income tax purposes, business owners typically prefer to classify payments as tax-deductible wages. This allocation reduces both their corporate taxes and their federal taxable income. As one might imagine, the IRS is correspondingly meticulous in its examination of these classifications. If it believes that owner compensation is excessive, it may claim that non-deductible dividends have been disguised as compensation. As they pertain to business valuation, the determination and application of reasonable shareholder-employee compensation are similarly contentious. The correlative relationship between owner compensation and cash flow means that when compensation is inflated, the available cash flow is reduced. Correspondingly, the indicated value under the income approach will be likewise reduced. But whether challenges to owner compensation emanate from taxing authorities or a rival valuation expert, the case law in this area strongly indicates that there is no global rule of thumb – reasonable officer compensation is determined according to the particular circumstances of an individual case. It is for this reason that Trial and Appellate Courts often struggle to resolve questions regarding reasonable officer compensation. For non-valuation professionals, this confusion is perhaps attributable to the number and diversity of sources used to ascertain reasonableness. […]